Afraid to Spend Money in Retirement? The Retirement Income Strategy That Gives You Permission

Quick Answer: What is Retirement Spending Anxiety?

Retirement spending anxiety is the psychological difficulty many retirees face when spending their accumulated wealth, even when they have sufficient funds. This article explains the three-layer retirement income strategy that eliminates this anxiety by separating guaranteed income from growth capital, giving retirees permission to spend without fear.

If you're sitting on $2 million or more and still can't bring yourself to spend $25,000 on the vacation you've dreamed about for 40 years, read every word of this article. What you're about to discover could be worth more than another decade of accumulation—it could give you back the life you've been postponing. This is a guide to overcoming the fear of spending in retirement.

The Retirement Spending Dilemma: David's Story

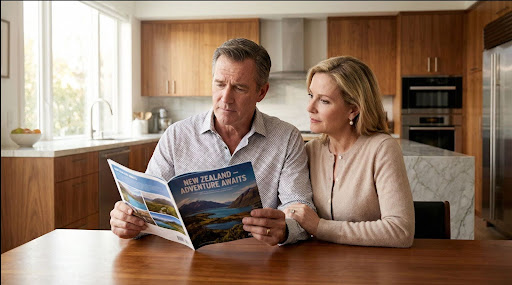

David sits at his kitchen table, coffee gone cold, staring at the brochure.

New Zealand. Three weeks. First-class. The trip his wife Susan has mentioned every year for the past decade. The one they've been "planning" since their 30th anniversary. The one that keeps getting postponed.

The package costs $28,000.

David has $3.2 million in the bank.

The math is absurd. Ridiculous. He could buy this trip 114 times over and still have more money than most people see in a lifetime. His advisor told him last month he's "more than fine." He could probably spend $120,000 a year and never run out.

But his hand won't move toward the phone.

His chest tightens. That familiar knot. The same one that shows up when Susan suggests replacing the 15-year-old car. When his daughter asks him to help with the grandkids' college fund. When his friend texts about playoff tickets.

What if the market crashes?

What if we need this money for healthcare?

What if I'm wrong about having enough?

The brochure sits there, mocking him. Beautiful photos of mountains and beaches and freedom. Things other people—people with less money than him—somehow feel entitled to enjoy.

He's 67 years old. He worked for 42 years. He did everything right. He has more money than he ever imagined possible.

And he feels like he's in prison.

Susan walks into the kitchen, sees the brochure, sees his face. She doesn't say anything. She's learned not to. She just pours her coffee and sits down across from him.

The silence between them weighs a thousand pounds.

You Know This Feeling (Don't Pretend You Don't)

Maybe your name isn't David. Maybe your number isn't $3.2 million. Maybe your dream isn't New Zealand.

But you know that knot.

You've felt it when you see something you want and immediately think: That's too much. I shouldn't. What if I need this money later?

You've experienced that nauseating guilt when you spend money on yourself—even though the spreadsheet says you can afford it, even though your advisor says you're fine, even though you've earned it a hundred times over.

You've had that fight with your spouse. The one where they say "When is it finally our time?" and you say "You don't understand how markets work" but what you really mean is: "I'm terrified and I don't know how to stop being terrified."

You've looked at your account balance—$2 million, $3 million, $5 million—and instead of feeling wealthy, you've felt anxious. Because somehow, no matter how big the number gets, it never feels like enough.

And the worst part? You can't talk about it. Because who's going to sympathize with someone who has millions in the bank but can't enjoy it? So you suffer in silence, feeling broken, weak, irrational.

Here's what I need you to understand: You are not broken.

This isn't a character flaw. This isn't weakness. This isn't irrationality.

This is architecture.

Why Retirement Planning Fails: The Portfolio Withdrawal Problem

Let me tell you what's really happening to you—the thing no one has bothered to explain.

For 40 years, you were taught to accumulate. Save more. Spend less. Delay gratification. Build the number. The entire system—from your first paycheck to your last 401(k) statement—trained you that spending threatens survival.

Every financial decision you made reinforced this: Money going out = danger. Money staying in = safety.

You internalized this so deeply it became your operating system. Your brain literally wired itself around this equation. It wasn't a choice. It was conditioning. Forty years of Pavlovian training.

Then one day, someone tells you: "Congratulations! You've won. You can retire. You have enough. Go enjoy it."

And they expect you to just... reverse 40 years of programming? With a mindset shift? With positive thinking?

That's not how brains work.

You can't undo four decades of survival wiring by deciding to "just relax." That's like telling someone with a phobia to "just stop being afraid." The fear isn't rational—it's neurological.

Here's the truth about your prison:

Your current plan requires you to spend from the same pool of money you've been trained to protect. Every time you withdraw money for living expenses, your brain registers it as a threat. Even if logically you know you can afford it, the emotional alarm bells ring.

This is called portfolio-consumption architecture—and it's the invisible prison keeping you locked up.

You have a $3 million portfolio. Your advisor says "withdraw 4%." So you take out $120,000 a year to live on.

But here's what your brain experiences:

Portfolio was $3,000,000.

Now it's $2,880,000.

The number went down.

Down = danger.

You lost $120,000.

Then the market drops 15% and your portfolio falls to $2,450,000. Now you're supposed to withdraw another $120,000 for next year's living expenses?

This brings you to $2,330,000.

You've "lost" $670,000 in 18 months.

Danger. Danger. Danger.

So you don't take the New Zealand trip. You don't replace the car. You don't help with college. You don't do anything that might accelerate the decline.

You survive. You don't live. You just... survive.

And every spreadsheet your advisor shows you saying "you're fine" doesn't change the feeling in your chest. Because the feeling isn't about the math. It's about the architecture.

You can't feel safe spending from a pool you're supposed to be protecting.

This is the invisible prison. And until someone changes the architecture, you'll die in it—with millions unspent and a lifetime of experiences missed.

What Happens If You Don't Escape

Let me show you the trajectory you're on if nothing changes.

Year 1-5: You postpone. The New Zealand trip becomes "maybe next year." The new car becomes "the old one still runs." Your spouse grows quietly resentful. You tell yourself you're being responsible.

Year 6-10: Your health starts changing. Not dramatically, but enough. That hip isn't what it used to be. The long flights sound exhausting. New Zealand starts to feel unrealistic. You tell yourself "we can still do smaller trips." You don't do those either.

Year 11-15: Your friends start dying. Jim has a heart attack at 73. Carol gets diagnosed at 75. You go to funerals and hear the same thing: "They had big plans. They were going to travel. They waited too long." You tell yourself you'll start living soon. You don't.

Year 16-20: You're 87 now. Susan is 85. She stopped asking about trips a decade ago. The account has $4.2 million—even after your conservative spending and a couple of market crashes, it grew. You won. You succeeded at accumulation. You sit in your paid-off house, looking at your seven-figure statements, and feel... nothing. Not joy. Not security. Just a vague sense of: I wasted it.

Year 21: Susan dies. You're alone with $4 million. The financial advisor says congratulations, you managed your money well. Your kids inherit $2.3 million after taxes. They use it to take their families to New Zealand. They post pictures. You see them from the nursing home.

This is what happens when you stay in the prison.

You don't run out of money. You run out of time. You run out of life. You run out of the very thing the money was supposed to buy: freedom.

And the tragedy—the absolute gut-wrenching tragedy—is that it didn't have to be this way.

The Day Everything Changed For David

I need to tell you what happened to David.

Six months after that kitchen table moment, David found himself in our office. He didn't come willingly. Susan made the appointment. She'd reached her breaking point after he said no to their 40th anniversary party because "that's a lot of money for one night."

David sat across from me with his arms crossed, ready to hear another lecture about 60/40 portfolios and safe withdrawal rates and staying the course. He'd heard it all before. None of it had helped.

I didn't start with his portfolio. I started with a question:

"David, if I could show you a plan where your lifestyle income was completely guaranteed for life—where markets could crash 50% and your monthly paycheck would still arrive like clockwork—would that change how you feel about spending money?"

He stared at me. "That's... is that possible?"

"What if," I continued, "you had a separate pool of money designated specifically for enjoyment—for New Zealand, for cars, for spoiling grandkids—and I could prove to you mathematically that you could drain that entire pool to zero without it affecting your income or leaving your kids with less than you planned?"

His eyes watered. "I don't understand."

"David, the problem isn't that you don't have enough money. The problem is that your money isn't organized to give you permission. Your brain is doing exactly what it's supposed to do given your plan's architecture. Let me show you a different architecture."

I pulled out a single sheet of paper.

The Three-Layer Retirement Income Strategy: Guaranteed Income for Life

Here's what I showed David. This is the structure that changed everything:

LAYER 1: SAFETY ($120,000)

Six months of living expenses in cash and money market.

Purpose: Emotional comfort. Immediate access. Zero market exposure.

This layer exists for one reason: so you can sleep at night knowing you have a cushion.

LAYER 2: INCOME ($800,000)

Generates $60,000/year in guaranteed lifetime income.

Purpose: Replace your paycheck. Forever.

This layer is constructed from:

Social Security: $36,000/year

Income annuities: $24,000/year (from $400,000)

Structured notes and bonds: (remaining $400,000 generating income)

This income continues regardless of:

Market crashes

How long you live

What you spend from other layers

Whether you're 70, 80, 90, or 100 years old

Your lifestyle is secured. Permanently.

LAYER 3: POSSIBILITY ($2,280,000)

This is the money that changes everything.

This layer has one job: fund your dreams and grow your legacy.

Here's what makes it magical: You can drain this to zero and your lifestyle doesn't change at all.

Your $60,000/year from Layer 2 keeps coming. Your safety cushion in Layer 1 is untouched. Your life goes on exactly the same.

Which means every dollar in this layer is permission money.

Want to spend $80,000 on a New Zealand trip? Pull it from Layer 3. The layer drops to $2,200,000. Your income? Still $60,000/year.

Want to buy a $70,000 truck? Layer 3 becomes $2,130,000. Your income? Still $60,000/year.

Want to help grandkids with college? $100,000 distributed. Layer 3 is now $2,030,000. Your income? Still. The. Same.

Do you see what this does psychologically?

Your brain stops registering spending as a threat. Because spending from Layer 3 doesn't threaten Layer 2 or Layer 1. The things that protect you are completely separate from the things that provide enjoyment.

The internal war stops.

The equation changes from: "Spending = threatening my security"

To: "Spending = using the freedom fund without touching security"

When David saw this, he wept.

Not because the numbers were different. His total net worth was the same $3.2 million.

He wept because for the first time in 40 years, he had permission.

What Happened Next

David and Susan went to New Zealand.

They stayed four weeks instead of three. They upgraded to first class. They did the helicopter tours and the luxury lodges and the wine country experiences. They spent $42,000.

David told me it was the first vacation in his entire life where he didn't check his account balance every day. The first time he ordered wine without looking at the price. The first time Susan looked at him without that quiet disappointment in her eyes.

When they got back, I asked him how it felt.

He said: "I kept waiting for the fear to come. For the panic. For the guilt. It never did. I'd look at Susan laughing at something and think: 'This is what it was all for. This is why I worked for 42 years. Not to watch a number grow. To watch her laugh in the New Zealand sunshine.' I can't believe I almost died without experiencing this."

Layer 3 went from $2,280,000 to $2,238,000.

His income remained $60,000/year.

His life became immeasurably richer.

But here's the part that shocked him:

Over the next three years, while spending $130,000/year on life (far more than he'd ever spent), Layer 3 didn't shrink. It grew.

Because Layer 3 wasn't being interrupted by withdrawals for living expenses. It could be positioned aggressively. It could compound uninterrupted. It could recover from dips because he wasn't forced to sell during crashes.

By year three, despite spending $390,000 on living fully, Layer 3 had grown to $2,650,000.

He was spending more. Enjoying more. And becoming wealthier.

And his kids? We'd secured $2 million in tax-free life insurance for them. They were going to inherit more than if David had hoarded every penny.

He won every way it's possible to win.

The architecture did what 40 years of discipline could not: It gave him permission to live.

Why You've Never Seen This Before

You might be wondering: If this is so powerful, why hasn't my advisor shown me this?

Fair question. Painful answer.

Most financial advisors can't design this because they don't understand the problem they're solving.

They think you need better returns. You don't.

They think you need a higher risk tolerance. You don't.

They think you need to "just spend more." You can't.

What you need is architecture that speaks to your nervous system, not just your spreadsheet.

You need someone who understands that retirement planning isn't portfolio optimization—it's behavioral engineering.

And here's the thing most advisors will never tell you:

They're terrified of this conversation. Because admitting that your problem is architectural means admitting that everything they've been doing—the portfolio tweaking, the rebalancing, the performance reports—doesn't solve your actual problem.

They're selling performance. You need permission.

It's not a fit.

At Virtus, we start with the problem you actually have: You're in a prison of your own wealth and you need architecture to break free.

Everything we build flows from that understanding.

The Five Pillars of Retirement Income Planning

The Three-Layer Strategy sits inside a larger framework we call the Five Pillars of Possibility Planning. Each pillar addresses one fundamental requirement of retirement:

1. REPLACE IT

Your income doesn't stop when your paycheck does. We engineer guaranteed lifetime income that replaces what you earned while working. This is Layer 2—your security foundation.

2. PROTECT IT

We eliminate the risks that destroy retirement plans: market crashes, RMD tax bombs, healthcare shocks, inflation, longevity risk. We design for the downside first. Then we capture upside.

3. GROW IT

With income secured (Layer 2) and spending separated (Layer 3), your growth capital can compound uninterrupted. No forced selling. No panic. Pure compounding for 20-30 years.

4. ENJOY IT

This is Layer 3—your permission architecture. Money you can spend freely because it doesn't threaten anything else. This is why we do all of this. Not to die rich. To live fully.

5. LEAVE IT

We use life insurance to lock in what your kids receive. This frees you to spend Layer 3 guilt-free. Result: You enjoy more, kids inherit more. Everyone wins.

These five pillars interlock. Each supports the others.

Replace stabilizes lifestyle.

Protect eliminates shocks.

Grow compounds uninterrupted.

Enjoy is safeguarded.

Leave becomes larger and cleaner.

This is how we engineer freedom from the prison.

What Changes When You Have This

I want you to imagine your life 90 days after implementing this plan.

You wake up on a Tuesday. Your $5,000 monthly income arrived automatically yesterday—like it does every month, like it will for the rest of your life.

Your spouse mentions that trip to Italy. Your stomach doesn't tighten. You don't change the subject. You say: "Let's book it."

You see your account statement. Layer 3 dropped from $1.8M to $1.75M after funding some upgrades and experiences. You notice it. You don't care. Because Layer 2 is still generating your $5,000/month. Layer 1 still has your $100k safety cushion.

The number went down and you feel... nothing. No alarm bells. No panic. No guilt.

Because the architecture has separated security from enjoyment.

Your grandkids ask you to go to Disneyland with them. You say yes immediately. You pay for the whole family. You spend $15,000. It's the best week of your life.

At Christmas, your son mentions his roof needs replacing. It's $22,000. In the past, you'd have said "that's what emergency funds are for" while feeling sick about it. Now you write the check. Layer 3 adjusts. Your income doesn't.

Your daughter wants to start a business. She needs $50,000. You invest in her dream. You cry when she hugs you and says "thank you for believing in me." Layer 3 doesn't care. Your lifestyle doesn't change.

This is what architecture makes possible.

Not just financial security. Not just theoretical freedom.

Actual, tangible, lived freedom.

The freedom to say yes.

The freedom to be generous.

The freedom to experience life instead of surviving it.

The freedom to look your spouse in the eye without shame.

The freedom to die with memories instead of money.

And here's the beautiful part: While you're living this way, your wealth keeps growing.

Because Layer 3 isn't being interrupted. It's compounding. It's working. It's doing what growth capital is supposed to do.

In 10 years, you've spent $500,000 on living fully—and Layer 3 has grown to $2.4M.

You've won in every possible dimension.

Your kids are getting $2M tax-free when you die.

You've lived a life worth living.

Your marriage is stronger.

Your grandkids have memories of a grandparent who said yes.

This is the transformation.

From prisoner to free person.

From surviving to thriving.

From fear to possibility.

Frequently Asked Questions About Retirement Income Planning

Q: What is retirement income planning? A: Retirement income planning is the process of creating guaranteed lifetime income to replace your paycheck in retirement. Unlike portfolio management, which focuses on growth, income planning focuses on creating reliable cash flow that won't run out, regardless of market conditions.

Q: How much can I safely spend in retirement? A: The traditional 4% rule suggests withdrawing 4% of your portfolio annually. However, the three-layer strategy separates your wealth into safety, income, and possibility layers, allowing you to spend from your possibility layer without threatening your guaranteed income. This often allows for higher spending rates (5-7%) with lower risk.

Q: What is guaranteed lifetime income? A: Guaranteed lifetime income is cash flow that continues for your entire life, regardless of market performance or how long you live. It's created through a combination of Social Security, pensions, annuities, and structured income products. This forms the foundation of the three-layer strategy.

Q: How do I overcome fear of spending in retirement? A: Fear of spending stems from portfolio-consumption architecture, where spending threatens the same pool you're trying to protect. The solution is architectural: separate your guaranteed income (Layer 2) from your spending money (Layer 3). When spending doesn't threaten your income, the fear disappears.

Q: What is the three-layer retirement strategy? A: The three-layer strategy separates your wealth into: Layer 1 (Safety: 6 months cash), Layer 2 (Income: generates guaranteed lifetime income), and Layer 3 (Possibility: growth and discretionary spending). This architecture eliminates the psychological conflict between spending and security.

The Conversation We Need To Have

I know what you're thinking right now.

Part of you is feeling hope—maybe for the first time in years. The possibility that there's a way out of this prison.

Part of you is scared. Skeptical. Thinking: This sounds too good. What's the catch? Why haven't I heard about this before?

Part of you is already making excuses: This probably won't work for my situation. I'm different. My advisor has a good plan. I should just try harder to relax.

I need you to hear me very carefully:

You have been carrying this weight alone for too long.

That knot in your stomach when your spouse suggests spending money? That's not normal. That's not just "being responsible." That's a prison sentence.

That guilt when you consider doing something nice for yourself? That's not virtue. That's trauma from 40 years of programming that was necessary when you were building but is now destroying what you built.

That fear that keeps you up at night even though you have millions in the bank? That's not paranoia. That's what happens when your plan architecture creates constant perceived threat.

None of this is your fault.

But continuing to live this way when there's an alternative? That becomes a choice.

Here's what I know:

You've worked too hard and sacrificed too much to die in this prison.

You've earned the right to live freely.

Your spouse deserves to see you relaxed and joyful instead of anxious and withdrawn.

Your grandkids deserve a grandparent who says yes instead of one who's always calculating.

Your future self—the 85-year-old version of you looking back on these years—deserves to remember experiences and laughter instead of regret and missed opportunities.

You deserve freedom.

Not the theoretical freedom of a large bank balance.

Actual, lived freedom.

And I'm telling you with absolute certainty: The architecture exists to give you that freedom.

The Three-Layer Strategy is real.

The Five Pillars are proven.

The transformation is possible.

But you have to take the first step.

Your Invitation to Freedom

We call it a Possibility Planning Session.

It's 45-60 minutes where we sit down together and do something radical: We tell the truth about where you are.

Not where the spreadsheet says you should be. Where you actually are.

We talk about:

The knot in your stomach

The fights with your spouse

The dreams you've been postponing

The fear that won't go away no matter what your account balance says

Then we diagnose why you feel this way.

We map your income gap. We show you exactly how much guaranteed income you'd need to feel secure.

We design your Three-Layer Strategy with your actual numbers.

And we show you what your life looks like on the other side of this transformation.

This is not a sales pitch.

I'm not trying to convince you that you need us.

I'm trying to show you that you don't have to live in this prison.

At the end of our session, you'll have:

Some people leave that session and implement this with their current advisor (though most advisors can't execute it). Some people choose to work with us. Some people need time to process.

All of that is fine.

What's not fine is continuing to suffer in this prison when the door is unlocked.

David sat where you're sitting right now—reading this, feeling that mixture of hope and skepticism, wondering if this could really be true for him.

Three months later he was in New Zealand, laughing with his wife, living the life he'd earned.

The only difference between David then and David now was one decision:

He booked the session.

The Choice In Front of You

You can close this page right now and go back to your life.

The Italy trip will get postponed again. The new car will stay in the dealership. The grandkids will grow up wondering why grandpa never seemed happy. Your spouse will stop asking. You'll die with millions and regrets.

Or you can do something different.

You can acknowledge that what you've been doing isn't working—not because you're doing it wrong, but because the architecture is broken.

You can admit that you need help with something you can't fix alone.

You can take 45 minutes to explore whether there's a better way.

Forty-five minutes.

That's all I'm asking.

Forty-five minutes to see if the prison door is actually unlocked.

Forty-five minutes to discover if freedom is possible.

Forty-five minutes that could change the entire trajectory of the next 20-30 years of your life.

David's session was on a Thursday. Three months later, he sent me a photo from New Zealand—him and Susan at the top of some mountain, arms around each other, faces lit up like teenagers.

The caption said: "Thank you for giving me my life back."

I think about that photo sometimes. About how close David came to never experiencing that moment. How close he came to dying without ever feeling free.

Don't let that be your story.

You've earned freedom. You've paid for it with 40 years of discipline and sacrifice.

All that's left is to build the architecture that allows you to claim it.

Book Your Possibility Planning Session

This is your moment.

The moment where you stop surviving and start living.

The moment where you choose freedom over fear.

The moment where you unlock the prison you didn't even know you were in.

Click the button below. Pick a time. Show up.

Forty-five minutes from now, you could be looking at the blueprint for the rest of your life—a life lived in possibility instead of anxiety, in freedom instead of fear, in joy instead of just-in-case.

David did it.

Susan got her New Zealand trip.

Their grandkids got a grandpa who says yes.

Their future selves avoided a lifetime of regret.

Now it's your turn.

[BOOK YOUR POSSIBILITY PLANNING SESSION NOW]

P.S. — If you're still reading this, you know something needs to change. Trust that instinct. The feeling that brought you to this article is the same feeling that's been trying to tell you for years: "There's got to be a better way."

There is.

And it starts with one conversation.

Book it now. Before you talk yourself out of it. Before the fear wins again. Before another year passes and you're still in the same prison.

Your future self—the one laughing in New Zealand or hugging grandkids at Disneyland or driving that truck you've always wanted—is counting on you to make this call.

Don't let them down.

[BOOK YOUR SESSION — IT TAKES 60 SECONDS]

Virtus Financial Planning

Where possibility becomes reality.

References

[1] Social Security Administration [2] Morningstar [3] Journal of Financial Planning [4] Internal Revenue Service (IRS)

About the Author

Andrew Hall, CPA is the founder of Virtus Financial Group, a financial planning firm specializing in retirement and tax planning strategies for high-net-worth individuals. With over 20 years of experience as both a CPA and financial advisor, Andrew helps clients navigate the complex intersection of retirement planning and tax strategy to maximize wealth preservation and minimize lifetime tax burdens.